Dehydrated Money

Why Your Fintech Product Is Useless Until the Funds Actually Move

I saw a gag gift recently: a 16oz can of “Dehydrated Water.” Instructions: Just Add Water. The label promises it’s 100% organic, BPA-free, low-sodium, and — my favorite — “Yes, This is Real.”

I laughed. Then I stopped laughing, because I realized I’ve shipped this product. Most of us in fintech have.

A checking account where your paycheck “arrives” but sits on hold? Dehydrated water. A P2P app that says “Sent!” while the recipient’s bank stares at the ceiling until Tuesday? Dehydrated water. A “real-time” dashboard showing a balance you cannot actually spend? That’s not a product. That’s a can with a very confident label.

Here’s the uncomfortable truth I learned building a consumer banking product from zero: a payment that hasn’t settled is not a payment. It’s a promise wearing a payment’s clothes. And customers can tell the difference, even when our marketing copy can’t.

The “Just Add Water” problem in U.S. payments

For decades, American money movement has been a beautifully labeled can. ACH batches. Two-to-three business days. “Business days” — a phrase that assumes your rent, your payroll emergency, and your kid’s field trip fee all politely occur Monday through Friday, 9 to 5.

Meanwhile, the actual ingredient — money you can use right now — was missing. We compensated with engineering duct tape: provisional credits, hold strategies, risk models predicting whether a deposit would “probably” clear. I’ve personally spent quarters of roadmap on ACH hold logic. Quarters. We were optimizing the label instead of putting water in the can.

The rest of the world already added the water

While the U.S. debated, two countries ran the experiment at civilization scale:

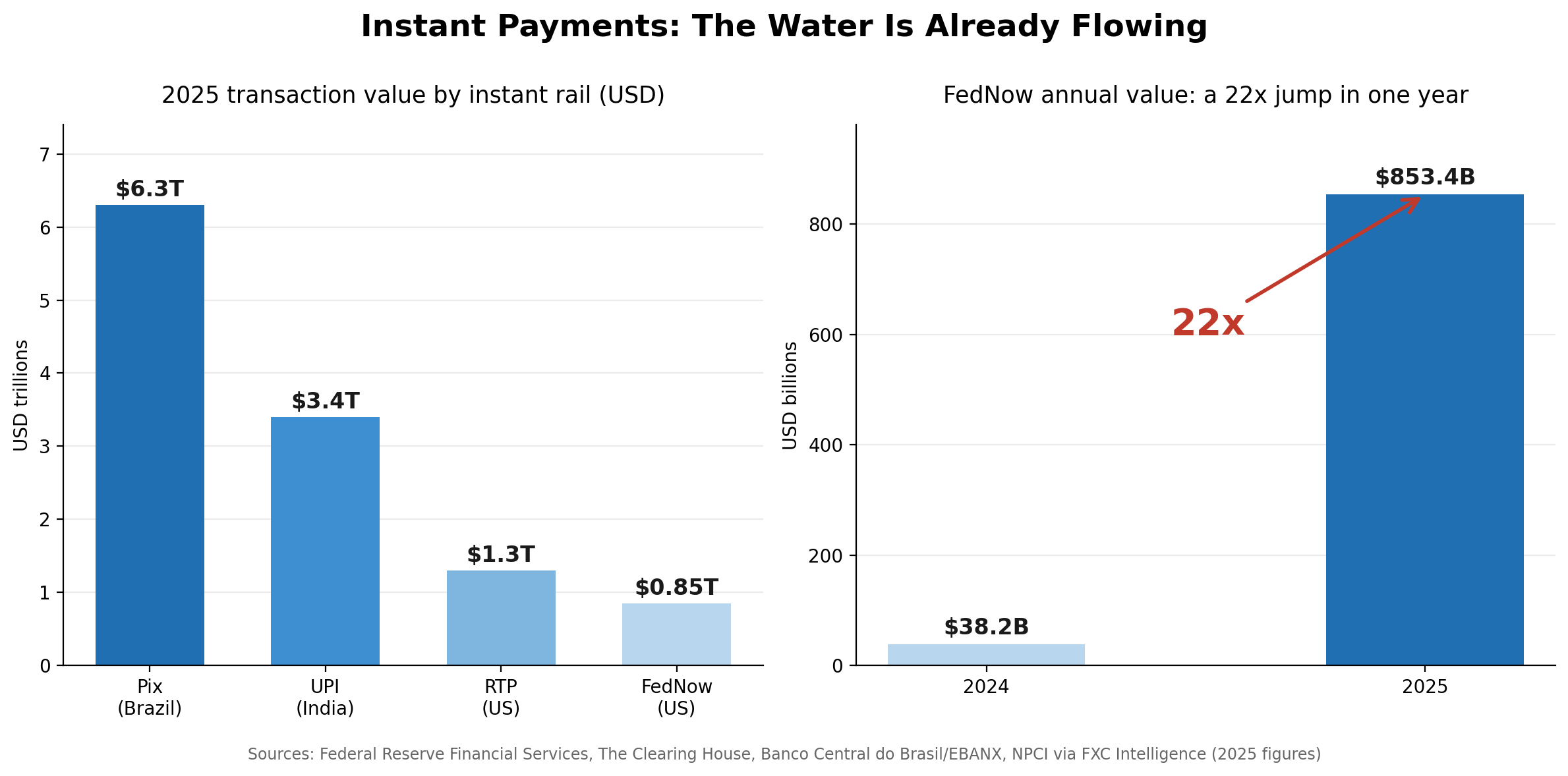

Brazil’s Pix processed roughly 79.7 billion transactions worth about $6.3 trillion in 2025, up 34% year over year — and it’s barely five years old. It’s approaching 8 billion transactions a month.

India’s UPI handled about 228.3 billion transactions in 2025, worth roughly $3.4 trillion. Street vendors selling chai accept instant account-to-account payments more reliably than some U.S. enterprise SaaS companies collect invoices.

These aren’t pilots. They’re the default way two of the world’s largest economies move money. The lesson is brutal in its simplicity: when money moves instantly, people move more money. Velocity isn’t a feature. It’s the product.

And now the U.S. can is finally filling up

The American numbers are smaller — but look at the slope, not the intercept:

FedNow went from $38.2 billion in transaction value in 2024 to $853.4 billion in 2025 — a 22x jump in one year, with over 1,600 financial institutions on the network and the transaction cap now raised to $10 million.

RTP (The Clearing House) processed more than $1.3 trillion in 2025 across 1,100+ banks and credit unions, also with a $10 million cap.

Industry forecasts suggest instant payments could represent ~25% of all U.S. electronic payment volume within three years.

When the Fed raises a transaction cap from $1 million to $10 million, that’s not consumer Venmo-for-pizza behavior. That’s corporate treasury, real estate closings, payroll, and supplier payments quietly migrating to rails that don’t take weekends off.

Why product managers should care (beyond the demo)

Instant settlement isn’t a speed upgrade. It changes the economics of everything downstream:

1. Holds become a choice, not a necessity. Every dollar sitting in a provisional-credit limbo is customer trust evaporating. Instant rails let you redesign onboarding, funding, and first-transaction experiences around confirmed money. Activation rates follow.

2. Fraud changes shape — and you must too. Irrevocable + instant means your fraud controls move from “review queue” to “milliseconds.” This is the hard part nobody puts on the label. If your risk stack was built for batch, instant payments will find that out for you, in production, at 2 a.m. on a Sunday.

3. The orchestration layer becomes the battleground. With FedNow, RTP, same-day ACH, push-to-card, and (yes) stablecoins all coexisting, the winning products won’t bet on one rail. They’ll route — picking the fastest, cheapest, safest path per transaction. The rails are becoming plumbing. The routing intelligence is becoming the moat.

4. “Receive-only” is the new dehydrated water. Most U.S. institutions on instant rails today can receive but not send. That’s half a product. The institutions that enable send-side first will own the use cases — earned wage access, instant insurance payouts, gig payouts, account funding — while everyone else is still reading the instructions on the can.

The punchline

The can says “Makes Up to Infinite Gallons!” — and weirdly, that’s the one claim that holds up. Money that moves instantly gets moved more. Pix and UPI proved that demand for velocity is effectively bottomless once friction disappears.

So here’s my question for every fintech roadmap discussion this quarter: is your money-movement experience the water — or the can?

Because customers have stopped paying for labels. They just want to add water and have it already be there.

Warning: excessive di-hydrogen monoxide can be dangerous. Excessive settlement latency, more so. Consult your product manager before use.

If you want to buy gag gift, check it out here.

Sources: Federal Reserve Financial Services FedNow volume statistics; The Clearing House 2025 RTP figures; Banco Central do Brasil / EBANX Pix data; NPCI UPI data via FXC Intelligence; Digital Transactions; PaymentsJournal.